Call and Put OptionsConsumer Products

Call and put options are derivative investments. That means their price moves based on the price movements of another financial product.

Definition and Example of Call and Put Options

Options can be defined as contracts that give a buyer the right to buy or sell the underlying asset, or the security on which a derivative contract is based, by a set expiration date and at a specific price.

- A call option is bought if the trader expects the price of the underlying asset to rise within a certain time frame.

- A put option is bought if the trader expects the price of the underlying asset to fall within a certain time frame.

How Call Options Work

For U.S.-style options, a call is an options contract that gives the buyer the right to buy the underlying asset at a set price at any time up to the expiration date.

It is only worthwhile for the call buyer to exercise their option (and require the call writer/seller to sell them the stock at the strike price) if the current price of the underlying asset is above the strike price. For example, if the stock is trading at $9 on the stock market, it is not worthwhile for the call option buyer to exercise their option to buy the stock at $10, because they can buy it for a lower price on the market.

What the Call Buyer Gets

The call buyer has the right to buy a stock at the strike price for a set amount of time. For that right, they pay a premium. If the price of the underlying asset moves above the strike price, the option will have intrinsic value. The buyer can sell the option for a profit, which is what many call buyers do, or they can exercise the option (i.e., receive the shares from the person who wrote the option).

What the Call Seller Gets

The call writer/seller receives the premium. Writing call options is a way to generate income. However, the income from writing a call option is limited to the premium. A call buyer, in theory, has unlimited profit potential.

How to Calculate the Call Option’s Cost

One stock call option contract represents 100 shares of the underlying stock. Stock call prices are typically quoted per share. To calculate how much it will cost you to buy a contract, take the price of the option and multiply it by 100.

Call options can be in, at, or out of the money:

- “In the money” means that the underlying asset price is above the call strike price.

- “Out of the money” means that the underlying price is below the strike price.

- “At the money” means that the underlying price and the strike price are the same.

You can buy a call in any of those three phases. However, you will pay a larger premium for an option that is in the money, because it already has intrinsic value.

How Put Options Work

Put options are the opposite of call options. For U.S.-style options, a put options contract gives the buyer the right to sell the underlying asset at a set price at any time up to the expiration date.2 Buyers of European-style options may exercise the option—sell the underlying asset—only on the expiration date.

Here, the strike price is the predetermined price at which a put buyer can sell the underlying asset. For example, the buyer of a stock put option with a strike price of $10 can use the option to sell that stock at $10 before the option expires.

What the Put Buyer Gets

The put buyer has the right to sell a stock at the strike price for a set amount of time. For that right, they pay a premium. If the price of the underlying asset moves below the strike price, the option will have intrinsic value. The buyer can exercise the option and sell for a profit, which is what many put buyers do.

What the Put Seller Gets

The put seller, or writer, receives the premium. Writing put options is a way to generate income. However, the income from writing a put option is limited to the premium, while a put buyer can continue to maximize profit until the stock goes to zero.

Calculating the Put Option’s Cost

Put contracts represent 100 shares of the underlying stock, just like call option contracts. To find the price of the contract, multiply the underlying asset’s share price by 100.

Put options can be in, at, or out of the money, just like call options:

- “In the money” means that the underlying asset price is below the put strike price.

- “Out of the money” means that the underlying price is above the strike price.

- “At the money” means that the underlying price and the strike price are the same.1

Just as with a call option, you can buy a put option in any of those three phases, and buyers will pay a larger premium when the option is in the money, because it already has intrinsic value.

What A Call Option Is

A call option is a contract that gives the buyer of the option the right to purchase a security, such as a specific stock, at a specific price (referred to as the strike price). The other type of option is called a put option, which allows the option holder to sell a specific security asset at a specified strike price. Both types of options have expiry dates. Equity/Stock options are the most widely known by investors.

Many institutions deal in complex and unusual options on other types of financial securities. Call options can be bought and sold on a wide array of securities, including ETFs, bonds, interest rates, futures, indexes, currencies, and swaps.

Importantly, an investor who has bought a call option is not obligated to exercise it and purchase the underlying asset at the strike price. Investors have the choice whether and when they want to exercise options they own, or not exercise them. If, however, at expiry an option is in-the-money, the option will automatically be exercised at that time.

A distinction can be made between European-style options, which can be exercised only at expiry, and American-style options, which can be exercised at any time prior to expiry. In all cases though, options provide option buyers the opportunity to generate leveraged exposures to the underlying security.

How Call Options Are Created

A call option contract is created on a securities exchange when an option writer/seller transacts with an option buyer. The option seller (also called the option writer) gives the buyer of the option the right, but not the obligation, to acquire a specified quantity of a security, such as a certain stock at a specified price. For equity call options, the quantity of shares per contract is 100, which means that the buyer of 1 option contract can exercise that option to buy 100 shares of the underlying stock at the specified strike price.

The investor that buys a call option contract pays a price, called the option premium, to the writer/seller of the call option contract.

The Option Premium

The market value of options is determined by buyers and sellers, just like with stocks or other securities. However, options are derivatives of an underlying security.

In assessing fair option contract value consider:

- the strike price of the option

- the current price of the underlying security

- the time to expiry for the option

- the expected volatility of the underlying security

In considering these factors, buyers and writers/sellers of options establish a market for options. Frequently, but not always, options trade with much less liquidity than stocks, and the bid-ask spread may be wide on option prices. Limit orders are commonly used by options traders, although market orders are possible and feasible for options with smaller bid-ask spreads.

The option premium represents the price at which an option (a call or a put) is transacted between the option buyer and the option writer/seller.

How Call Options Work at Expiry

A call option will possess value at expiry if the price of the underlying security is above the strike price of the contract. In such a case, the call option is said to possess intrinsic value, or be trading in-the-money. Here, exercising the option would allow the option holder to buy the stock at a price that is lower than that stock’s current market price, benefitting from doing so.

For the option writer/seller, the intrinsic value of the call option at expiry represents a cost. The call option buyer has the right to purchase the underlying security at the strike price, and the call option seller is obligated to sell the underlying security at the strike price. If the market value of the security is higher than the strike price at expiry, the call option writer/seller is required to deliver the underlying security to the call option buyer below its market value. If the option writer/seller doesn’t already own the underlying security, they will have to purchase it at market value and then sell it below market value (at the strike price).

At expiry, the intrinsic value of a call option represents a benefit to the option buyer and a cost to the option writer/seller. The value of these will offset each other. For example, if a call option is worth $200 to the option buyer at expiry (or at any time), it is simultaneously a $200 liability to the option seller.

Profits and losses on call option positions involve 2 components:

- the option premium

- the intrinsic value at expiry (if held to expiry)

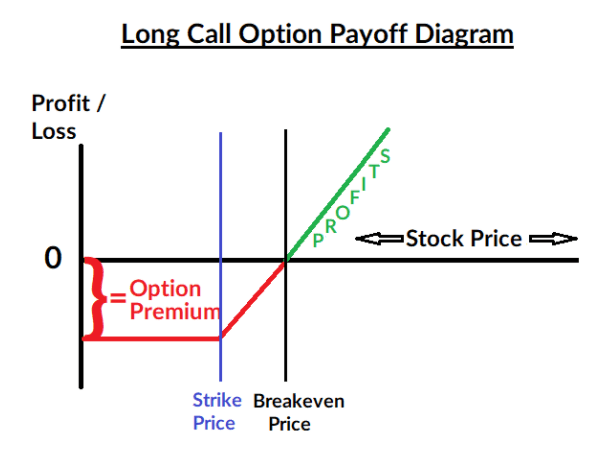

To determine the net profit of an options trade, option buyers can subtract the cost of the option premium from the intrinsic value at expiry. Even if an option expires in the money, the options buyer can suffer a net loss if the intrinsic value is less than the original cost of the option (the option premium). The breakeven price (see above diagram) is the point at which the intrinsic value of the option is equal to the option premium that was paid.

Once the breakeven point is reached, the higher the price of the call option, the greater the net profit will be for the option buyer. There is theoretically no upper limit to the price of the underlying security nor the potential profits for the option buyer.

The net profit/loss picture for the option writer/seller is effectively opposite that of the option buyer. If an option expires with an intrinsic value of $11/share, and the option premium was $4/share, the owner of the option has earned a net profit of $700 (1 contract = 100 shares), The option writer/seller will realize a net loss of $700 in this scenario, after receiving an option premium worth $4/share, but incurring an $11/share cost at expiry. Of course, any trade commissions or other fees incurred represent incremental costs.

- Option Buyer Profit (Loss) = Intrinsic value at expiry LESS option premium price

- Option Writer/Seller Profit (Loss) = Option premium price LESS Intrinsic value at expiry

Note: The above profit/loss formulas assume no commissions or fees are incurred

Call Option Example

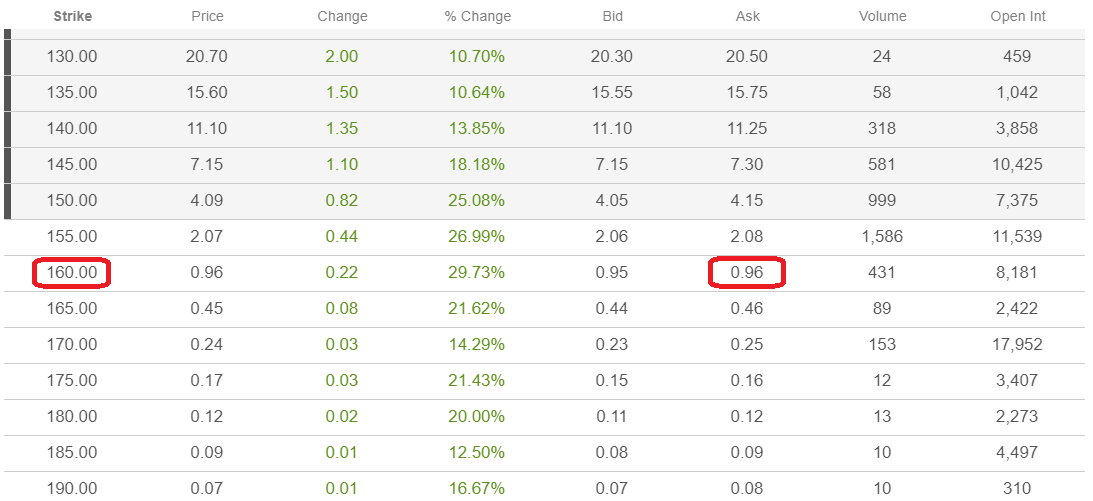

A call option trade could look like this. Let’s assume it’s October, and an investor believes that Walmart (WMT), whose stock is trading for $150/share, will have a widely successful Black Friday sales event that the market is not anticipating. In that case, the investor may want to buy a call option contract for Walmart stock that allows the investor to gain leveraged upside potential in case it turns out that Walmart does indeed have a stronger-than-expected Black Friday event, which would possibly result in a climbing share price. The current call option chain for Walmart, for options expiring mid-December, looks like this:

If the investor decides to acquire one contract with a strike price of $160, they will pay an option premium of $0.96 per share (the ask price), or $96 in total, for one option contract (which covers 100 shares of Walmart). The investor would then possess the right to buy 100 shares of Walmart at $160 each at any time through mid-December.

If, for example, Walmart shares were to trade at $165 by mid-December on the back of strong retail sales, the call option would have an intrinsic value of $5 per share and be worth $500 in total. After considering the cost of the option premium, the option buyer would realize a net profit of $404, excluding any commissions or fees. The writer of the call option, meanwhile, would suffer a net loss of $404.

If, however, Walmart does not trade above $160/share in mid-December, the option will expire worthless, and the option buyer will be out their $96 option premium. In this scenario, the option writer would pocket the $96 gain.

In an extreme scenario where Walmart shares close at $240/share in mid-December, the intrinsic value of the option would be $8,000. Here, the option writer would suffer significant losses at the hands of the option buyer.

Naked Call Writing vs Covered Call Writing

As seen above, options writing/selling can expose investors to significant losses. In fact, since there is no theoretical ceiling to the price of a security, writing call options exposes the investor to the potential for unlimited losses. Investors who write call options can protect against such potential losses by employing what’s referred to as covered call writing.

Investors who own shares of the underlying security can sell calls that are “covered”. In essence, they are protected against significant losses because they can deliver the underlying security from their holdings, should the call option be exercised against them.

Another way to view this is from the perspective that the covered call writer earns profits from the underlying security that they hold if it rises in value. The gains from holding the underlying security serve to offset the losses on writing/selling the call option (so long as the quantity of the underlying security owned is not fewer than the shares represented by the option. If an investor writes 2 call options on Walmart but owns 200 shares of Walmart stock, this investor is “covered”.)

Call option writers/sellers who do not own the underlying security are referred to as “naked call writers”.

Closing a Call Option Position Before Expiry

Both buyers and sellers of options contracts can seek to close out their option positions prior to the expiration date of the contract. The buyer of an option contract can eliminate the position by selling it, and the writer/seller of an option contract can close out the position by repurchasing the option they sold originally.

The transaction price of the closing trade will determine whether the buyer or writer/seller of an option has generated a profit or loss. If an option buyer closes their position at a higher price than the option was purchased for, a profit has been made. If an option seller closes their position at a lower price than the option was originally sold for, they will have made a profit.

- Option Buyer Profit (Loss) = Closing Trade (sell) Price – Original Purchase Price

- Option Writer/Seller Profit (Loss) = Original Selling Price – Closing Trade (buy) Price

Understanding Call Option Market Values

The market value of a call option will continue to change throughout the lifetime of the option as market participants adjust to changes in:

- the current price of the underlying security,

- the expected volatility of the underlying security, and

- the remaining time to expiry.

Prior to their expiration date, options (both calls and puts) typically trade for more than their intrinsic value. This is due to what’s called the time value of the option. If there is a lot of time remaining until the expiry date of an option, this means there is a lot of time for the underlying security price to move in favor of the option owner. As time passes, an option’s time value decreases. At expiry, an option will be worth its intrinsic value. The market value of an option is equal to the sum of its intrinsic value and time value.

Option Market Value = Intrinsic Value + Time Value

Call options should increase in value:

- If the underlying security increases, while expected volatility and time to expiration remain unchanged

- If expected volatility increases, while the underlying security price and time to expiration remain unchanged

Call options should decrease in value:

- If the underlying security decreases, while expected volatility and time to expiration remain unchanged

- If expected volatility decreases, while the underlying security price and time to expiration remain unchanged

- As time passes while the underlying security price and expected volatility remain unchanged

In reality, however, the underlying security price, expected volatility, and the time to expiration are often moving at the same time. The combination of these 3 elements contributes to the market’s determination of fair value for a call option. Investors who trade options may wish to utilize an option pricing model like Black Scholes.

Four Ways Investors Use Call Options

Speculating on a price increase

Investors that want to speculate on a price increase in an underlying security may benefit from buying call options on that security. While such an investor could alternatively just buy the underlying security, options offer leverage that increase potential % gains should the underlying security price move upward.

Investing using less capital

Call options can allow investors to gain exposure to a security using less capital. For instance, purchasing 100 shares of a $1,000 stock would require $100,000 in capital. As an alternative, investors could gain exposure to 100 shares of that same stock by purchasing 1 option contract for a much smaller cash outlay. WARNING: Call option prices include time value, which erodes as time passes. Investors of call options will suffer losses if the underlying security trades flat.

Exiting stocks at specific prices

An investor wishing to exit an existing stock position might choose to sell an option contract at a strike price equal to their take profit level. This can result in the generation of extra income, via option premiums, while waiting for the stock to reach the strike price. Note however that this investor remains exposed to losses on the underlying security from downward price movements.

Generating income by selling out-of-the-money covered calls

Investors wishing to generate income can regularly (or periodically) sell covered call options that are out of the money. By doing so, they can receive a steady stream of option premiums, so long as the underlying security doesn’t get called away. Investors trying to generate income through covered calls will often choose strike prices that are significantly higher than the current price of the underlying security, in order to minimize the likelihood of shares getting called away.

Contact us at the Consulting WP office nearest to you or submit a business inquiry online.

“I learned about the equity markets.

My experience with the company is memorable. The consultants are quite friendly. The research of Generali Finanza is really appreciable. I like the details research of the companies recommended. Thank You for your effort.”