- Luglio 2, 2024

- Posted by: Oliver

- Categoria: Economics, Finance & accounting

Lo slancio di SoFi non mostra segni di rallentamento

SoFi ha sostenuto un forte slancio entrando nell’anno fiscale 2024, senza mostrare segni di rallentamento. Nonostante il prezzo delle azioni suggerisca un peggioramento della performance, non è proprio così, con i ricavi in aumento del 37,5% a circa 645 milioni di dollari nei risultati più recenti del primo trimestre. Ciò è in linea con la crescita del trimestre precedente del 36,6%, non troppo lontana dalla crescita dello scorso anno del 46,1%.

Questi numeri superano di gran lunga quelli che si vedono oggi nel fintech. Prendiamo ad esempio PayPal (NASDAQ:PYPL), i cui ricavi sono aumentati del 9,4% nello stesso periodo. Altri, come Block (NYSE:SQ) e StoneCo (NYSE:STNE), hanno aumentato i loro ricavi rispettivamente del 19,4% e del 15,5%. Sebbene queste aziende differiscano nelle loro offerte e soluzioni, collettivamente dimostrano che la crescita di SoFi supera gli attuali standard di settore.

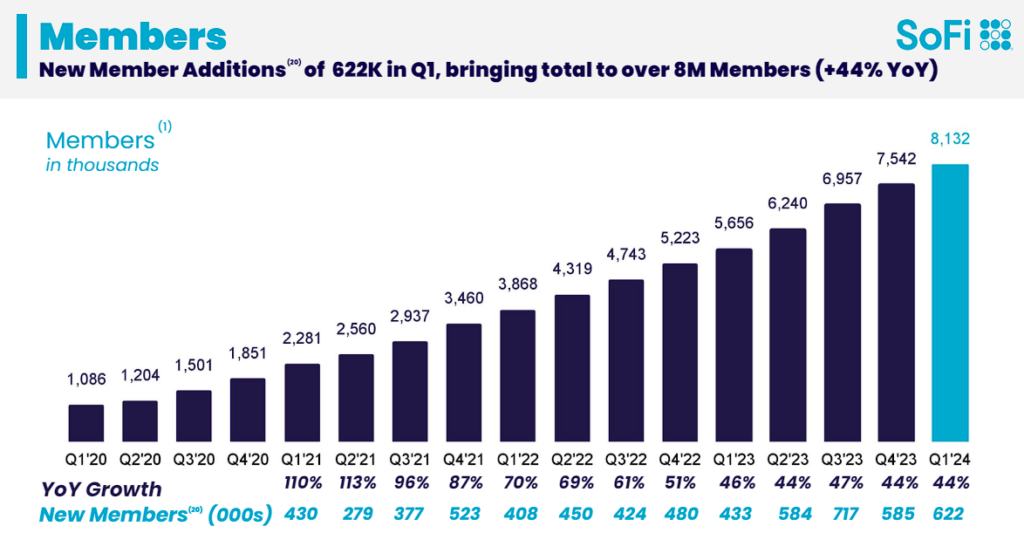

L’impressionante crescita di SoFi può essere attribuita principalmente alla sua crescente base di membri e al crescente numero di prodotti offerti sulla sua piattaforma. Il numero totale di membri ha raggiunto 8,1 milioni nel primo trimestre, in crescita del 44% rispetto allo scorso anno, con 622.000 nuovi membri che si sono uniti durante questo periodo. Questo tasso corrisponde all’aumento del 44% rispetto al trimestre precedente ed è vicino alla crescita del 46% dello scorso anno, suggerendo che il marchio SoFi rimane altamente rilevante e di tendenza nello spazio fintech. Inoltre, SoFi ha registrato 989.000 nuovi prodotti aggiunti nel trimestre, con un aumento del 38% rispetto al primo trimestre del 2023.

Fonte: presentazione per gli investitori del primo trimestre del 2024 di SoFi

L’espansione del margine stimola i profitti GAAP ed espone una valutazione conveniente

Con SoFi che sostiene una forte crescita dei ricavi e crea quindi spazio per migliorare le sue economie unitarie, la società sta per pubblicare il suo primo anno di utile netto GAAP. Fondamentalmente, SoFi ha ampiamente rafforzato il valore del proprio marchio e quindi non è più necessario fare pubblicità tanto quanto prima per ogni aggiunta incrementale di utenti. Pertanto, i suoi margini sono in aumento. Nel primo trimestre, ad esempio, le spese di vendita e marketing di SoFi sono state di 167,4 milioni di dollari, in calo rispetto a 175,2 milioni di dollari, senza sacrificare il potenziale di crescita degli utenti.

Pertanto, SoFi ha ottenuto un margine di utile netto GAAP positivo del 13,8%, continuando la tendenza positiva iniziata nel quarto trimestre del 2023. Dopo numerosi trimestri di margini negativi, SoFi ha dimostrato che il suo modello di business è, dopo tutto, altamente redditizio. In ogni caso, con margini positivi ora all’orizzonte, Wall Street prevede che l’anno fiscale 2024 sarà il primo anno GAAP redditizio per la società, con un utile per azione (EPS) destinato a sfiorare 0,08 dollari.

Naturalmente, si tratta di un piccolo profitto. Tuttavia, con la previsione che la crescita dei ricavi rimarrà a due cifre e i margini in rapida espansione, le stime di consenso sull’EPS nel medio termine sembrano particolarmente convincenti. Wall Street prevede un EPS di 0,23 dollari nell’anno fiscale 2025 e di 0,44 dollari nell’anno fiscale 2026.

Questi numeri mostrano che SoFi ha un prezzo molto interessante ai livelli attuali. A soli 14,5 volte le sue prospettive di EPS per l’anno fiscale 2026, sembra un multiplo molto conveniente, dato che la società sta prendendo d’assalto il settore. Certo, ci sono alcune speculazioni coinvolte qui, ma lo slancio di SoFi supporta fortemente questa valutazione.

Un altro motivo per cui adoro SoFi in questo multiplo è perché la diluizione dell’azienda è diminuita. Se SoFi stesse diluendo in modo aggressivo gli azionisti attraverso livelli significativi di compensi basati su azioni (SBC), come è comune nel settore, i suoi parametri di valutazione dovrebbero essere presi con le pinze. Tuttavia, il SBC di SoFi sta diminuendo sia in termini aggregati che in percentuale delle entrate. Nel primo trimestre è stato pari a 55,1 milioni di dollari, in calo rispetto ai 64,2 milioni di dollari dell’anno scorso e ai 77,0 milioni di dollari dell’anno precedente.

Le azioni SOFI sono da acquistare, secondo gli analisti?

Nonostante il suo prolungato calo, Wall Street sembra nutrire ancora sentimenti contrastanti riguardo al titolo. Nello specifico, SoFi Technologies ha raccolto una valutazione di consenso di Hold basata su quattro Buys, nove Hold e tre Sell assegnati negli ultimi tre mesi. A $ 8,35, l’obiettivo di prezzo medio delle azioni SoFi Technologies implica un potenziale di rialzo del 26,3%.

L’asporto

Nel complesso, il titolo SoFi sembra rappresentare un caso convincente dopo il suo continuo declino. Con una solida crescita dei ricavi, l’espansione dei margini e una base di membri in crescita nonostante la riduzione dei costi di marketing, è evidente che l’esecuzione del management è stata eccellente. Inoltre, dal momento che SoFi è ora redditizia su base GAAP, i rischi sono molto inferiori rispetto a un paio di anni fa, quando la società stava perdendo denaro.Con una forte prospettiva di EPS a medio termine e un prezzo delle azioni in calo, che hanno portato a una valutazione sempre più interessante, sembra il momento migliore per andare long sul titolo.

SoFi Technologies (NASDAQ:SOFI) stock has experienced a long decline over the past year, now trading near its 52-week low. The fintech platform for personal finance has lost about 24% of its value during this period despite the overall market reaching new highs by the week. This is a strange development, especially given that the company has sustained strong revenue growth and achieved considerable margin expansion. Given the contrast between SoFi’s financial performance and share price, I am bullish on the stock.

SoFi’s Momentum Shows No Signs of Slowing Down

SoFi sustained strong momentum entering Fiscal 2024, showing no signs of a slowdown. Despite the share price suggesting a deteriorating performance, this is hardly the case, with revenues rising by 37.5% to roughly $645 million in its most recent Q1 results. This is in line with the previous quarter’s growth of 36.6%, not too far from last year’s growth of 46.1%.

These numbers far exceed what you see in fintech today. Take PayPal (NASDAQ:PYPL), for example, whose revenues increased by 9.4% during the same period. Others, like Block (NYSE:SQ) and StoneCo (NYSE:STNE), grew their revenues by 19.4% and 15.5%, respectively. While these companies differ in their offerings and solutions, they collectively illustrate that SoFi’s growth surpasses current industry standards.

SoFi’s impressive growth can be mainly attributed to its increasing member base and the rising number of products offered on its platform. The total number of members reached 8.1 million in Q1, up 44% from last year, with 622,000 new members joining during this period. This rate matches the 44% increase from the previous quarter and is close to last year’s 46% growth, suggesting that SoFi’s brand remains highly relevant and trending in the fintech space. Also, SoFi reported 989,000 new product additions in the quarter, representing a 38% increase compared to Q1 2023.

Margin Expansion Drives GAAP Profits, Exposes Cheap Valuation

Thus, SoFi achieved a positive GAAP net income margin of 13.8%, continuing the positive trend that started in the fourth quarter of 2023. Following numerous quarters of negative margins, SoFi has shown that its business model is, after all, highly viable. In any case, with positive margins now on the horizon, Wall Street expects that Fiscal 2024 will be the first profitable GAAP year for the company, with earnings per share (EPS) set to land close to $0.08.

Of course, that’s a tiny profit. However, with revenue growth expected to remain in the double-digits and margins to keep expanding rapidly, EPS consensus estimates over the medium term seem particularly compelling. Wall Street sees EPS of $0.23 in FY2025 and $0.44 in FY2026.

These numbers show that SoFi is very attractively priced at its current levels. At just 14.5 times its FY2026 EPS prospects, it seems like a very cheap multiple, given that the company is taking the industry by storm. Sure, there is some speculation involved here, yet SoFi’s momentum strongly supports this assessment.

Another reason I love SoFi at this multiple is because the company’s dilution has been decreasing. If SoFi was aggressively diluting shareholders through significant stock-based compensation (SBC) levels, as is common in the space, its valuation metrics should be taken with a grain of salt. However, SoFi’s SBC is declining both in aggregate and as a percentage of revenue. It came in at $55.1 million in Q1, down from $64.2 million last year and $77.0 million the year before.

Is SOFI Stock a Buy, According to Analysts?

Despite its prolonged decline, Wall Street seems to still have mixed feelings about the stock. Specifically, SoFi Technologies has gathered a Hold consensus rating based on four Buys, nine Holds, and three Sells assigned in the past three months. At $8.35, the average SoFi Technologies stock price target implies 26.3% upside potential.

The Takeaway

Overall, SoFi stock seems to present a compelling case following its ongoing decline. With robust revenue growth, expanding margins, and a growing member base despite trimming marketing costs, it’s evident that management’s execution has been excellent. Furthermore, with SoFi now being profitable on a GAAP basis, there is much less risk involved compared to a couple of years ago when the company was losing money. With a strong EPS medium-term outlook and a declining share price, which have resulted in an increasingly attractive valuation, it seems like a prime time to go long on the stock.