- Novembre 18, 2022

- Posted by: Oliver

- Categoria: Economics, Finance & accounting

Tyson Foods (NYSE:TSN) stock has been on a roller coaster ride recently. The stock is down almost 2% over the past week. While the dip may appear small, it is indeed big compared to the 8.2% overall gains registered by the Nasdaq Composite over the same period.

Last week, Tyson Foods’ CFO John Tyson was arrested on charges of misconduct, intoxication, and trespassing after he was found asleep in a stranger’s home in a state of inebriation.

On November 14, the company delivered a mixed fiscal Q4 earnings bag, topping sales expectations but failing to meet earnings estimates. Q4 adjusted earnings came in at $1.63 per share versus $2.30 in the same period last year and also fell short of Street estimates of $1.70 per share.

The company made efforts to win back investors’ confidence by presenting impressive operational data. CEO Donnie King stated that consumer demand for protein remained robust, with “historically strong operations” in the Beef segment and improved performance in the Chicken segment.

He added, “We also experienced share gains in both our foodservice Focus 6 categories and retail core business lines, which include our Tyson, Jimmy Dean, Hillshire Farm, and Ball Park iconic brands.” For FY23, TSN expects revenues to range between $55 billion and $57 billion.

Is Tyson Publicly Traded?

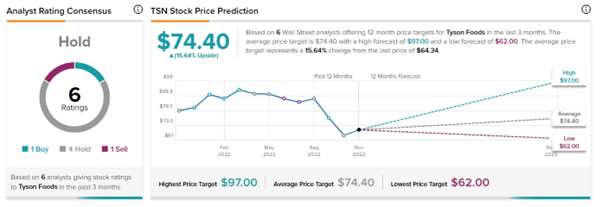

Tyson’s stock is traded under the symbol TSN on the New York Stock Exchange. Currently, analysts are cautious about Tyson Foods’ prospects, with a Hold consensus rating based on one Buy, four Holds, and one Sell. Tyson’s average target price is $74.40, which implies 15.64% upside potential from the current level.

Conclusion: Cheap Valuation Signals a Buying Opportunity

Tyson’s stock has lost almost 30% of its market capitalization over the past six months. While the ongoing CFO controversy has reduced investors’ confidence in the stock, the stock’s underlying fundamentals remain intact.

Looking at valuations too, the stock is trading at a discount to the peer group as well as its own five-year historical P/E averages. Tyson is currently trading at a P/E ratio of 7x, reflecting a huge 60% discount to its peer group P/E of 19x. Further, it implies a 40% discount to its five-year average of 11.5x.

The discounted valuation, perhaps, presents a good buying opportunity.