- Luglio 27, 2022

- Posted by: Oliver

- Categoria: Economics, Finance & accounting

American Express (AXP) reported stronger-than-expected Q2 results, topping both earnings and revenue estimates, driven by robust demand and performance across all segments.

Furthermore, the company raised its FY2022 revenue outlook but reiterated its earnings outlook. Shares of the credit card company gained 1.9% on July 22 to close at $153.01.

AXP’s Q2 Beat

The company reported earnings of $2.57 per share, which impressively beat analysts’ expectations of $2.40 per share. However, it was lower than the reported earnings of $2.80 per share in the prior-year period.

Meanwhile, revenues gained 30.9% year-over-year to $13.4 billion and also exceeded consensus estimates of $12.4 billion.

The revenue gain reflects a surge in card member spending, which gained 30%, driven by robust demand for travel and entertainment globally.

Furthermore, the company added 3.2 million new proprietary cards during the quarter, driven by strong demand for its premium products.

AXP Raises Revenue Outlook for FY2022

Based on robust Q2 results, management raised the financial guidance for FY2022.

The company now forecasts revenues to grow by 23% to 25%, higher than the previously guided range of 18% to 20%.

However, the company continues to forecast adjusted earnings in the range of $9.25 per share to $9.65 per share, which is lower than the consensus estimate, which is pegged at $9.77 per share.

AXP CEO’s Comments

American Express CEO, Stephen J. Squeri, said, “We have been able to deliver exceptional results while navigating a complex macroeconomic environment because of a number of factors, including the scale and strength of our global customer base, the decisions we made through the pandemic and recovery to support our customers and seize on growth opportunities, and our continued focus on enhancing our value propositions and bringing new customers into the franchise.”

Looking confidently to the future, he further added, “As we look ahead, we remain confident in our ability to successfully execute against our long-term growth plan aspirations.”

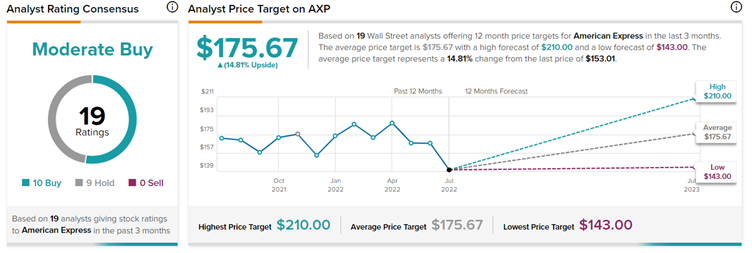

Wall Street’s Take on AXP

Despite upbeat results, CFRA decreased the price target on American Express to $190 (24.17% upside potential) from $210 and reiterated a Buy rating.

The rest of the Wall Street community is cautiously optimistic about the stock, with a Moderate Buy consensus rating based on 10 Buys and nine Holds. The average American Express price target of $175.67 implies 14.81% upside potential to current levels.

TipRanks’ Smart Score

AXP scores a 9 out of 10 on Smart Score rating system, indicating that the stock has strong potential to outperform market expectations.

Conclusion

Although AXP shares lost over 11% over the past year, they performed in-line with the benchmark indices.

The stock could be on the way to its upward trajectory as demand beat the pre-pandemic levels for the first time. The rebound in travel demand, as well as entertainment, resulted in strong revenue growth.

The positive demand indicators and resumed consumer credit card spending momentum bode well for the stock going forward.

American Express ( AXP ) ha riportato risultati del secondo trimestre più forti del previsto, superando sia le stime degli utili che dei ricavi, trainati dalla solida domanda e dalle prestazioni in tutti i segmenti.

Inoltre, la società ha aumentato le sue prospettive di fatturato per l’anno fiscale 2022, ma ha ribadito le sue prospettive di utili. Le azioni della società di carte di credito hanno guadagnato l’1,9% il 22 luglio per chiudere a $ 153,01.

Q2 Beat di AXP

La società ha registrato un utile di $ 2,57 per azione , che ha superato in modo impressionante le aspettative degli analisti di $ 2,40 per azione. Tuttavia, è stato inferiore all’utile riportato di $ 2,80 per azione nel periodo dell’anno precedente.

Nel frattempo, i ricavi sono aumentati del 30,9% anno su anno a 13,4 miliardi di dollari e hanno anche superato le stime di consenso di 12,4 miliardi di dollari.

L’aumento delle entrate riflette un’impennata nella spesa dei membri della carta, che è aumentata del 30%, trainata dalla forte domanda di viaggi e intrattenimento a livello globale.

Inoltre, la società ha aggiunto 3,2 milioni di nuove carte proprietarie durante il trimestre, trainata dalla forte domanda per i suoi prodotti premium.

AXP aumenta le prospettive delle entrate per l’anno fiscale 2022

Sulla base dei solidi risultati del secondo trimestre, la direzione ha alzato le linee guida finanziarie per l’esercizio 2022.

L’azienda prevede ora una crescita dei ricavi dal 23% al 25%, superiore all’intervallo precedentemente guidato dal 18% al 20%.

Tuttavia, la società continua a prevedere utili rettificati compresi tra $ 9,25 per azione e $ 9,65 per azione, che è inferiore alla stima di consenso, che è ancorata a $ 9,77 per azione.

Commenti del CEO di AXP

Il CEO di American Express, Stephen J. Squeri, ha dichiarato: “Siamo stati in grado di fornire risultati eccezionali mentre navigavamo in un contesto macroeconomico complesso grazie a una serie di fattori, tra cui la portata e la forza della nostra base di clienti globale, le decisioni che abbiamo preso attraverso il pandemia e ripresa per supportare i nostri clienti e cogliere le opportunità di crescita, e la nostra continua attenzione al miglioramento delle nostre proposte di valore e all’ingresso di nuovi clienti nel franchising”.

Guardando con fiducia al futuro, ha inoltre aggiunto: “Mentre guardiamo al futuro, rimaniamo fiduciosi nella nostra capacità di eseguire con successo le nostre aspirazioni del piano di crescita a lungo termine”.

La sfida di Wall Street su AXP

Nonostante i risultati positivi, CFRA ha ridotto l’obiettivo di prezzo su American Express a $ 190 (potenziale di rialzo del 24,17%) da $ 210 e ha ribadito un rating Buy.

Il resto della comunità di Wall Street è cautamente ottimista riguardo al titolo, con un rating di consenso di acquisto moderato basato su 10 acquisti e nove prese. L’obiettivo di prezzo medio di American Express di $ 175,67 implica un potenziale di rialzo del 14,81% rispetto ai livelli attuali.

Punteggio intelligente di TipRanks

AXP ottiene un punteggio di 9 su 10 nel sistema di valutazione Smart Score , indicando che il titolo ha un forte potenziale per sovraperformare le aspettative del mercato.

Conclusione

Sebbene le azioni AXP abbiano perso oltre l’11% nell’ultimo anno, hanno ottenuto risultati in linea con gli indici di riferimento.

Il titolo potrebbe essere sulla strada per la sua traiettoria al rialzo poiché la domanda ha battuto per la prima volta i livelli pre-pandemia. Il rimbalzo della domanda di viaggi, oltre che dell’intrattenimento, ha portato a una forte crescita dei ricavi.

Gli indicatori positivi della domanda e la ripresa della spesa per le carte di credito al consumo fanno ben sperare per il titolo in futuro.