- Aprile 6, 2022

- Posted by: Oliver

- Categoria: Economics, Finance & accounting

Shares of China-based cell therapy company Gracell Biotechnologies, Inc. (NASDAQ: GRCL) jumped 18.3% on Monday to close at $2.65 after BTIG analyst Justin Zelin initiated coverage on the stock with a Buy rating and a price target of $18, which reflects upside potential of 579.3% to current price levels.

Founded in 2017, Gracell is developing a pipeline of cell therapies to treat hematologic and solid tumor cancers. Its technology platform features TruUCAR to create differentiated allogeneic cell therapies and FasTCAR to reduce the manufacturing times of these therapies.

The analyst said that Gracell is “one of the most undervalued cell therapy companies with robust clinical data in high-risk relapsed/refractory multiple myeloma, an experienced management team, and a multi-asset portfolio targeting heme and solid tumor cancers.”

Why is Gracell Undervalued?

The company’s poor performance is primarily due to the overall underperformance of the biotechnology sector, Zelin said. He added that the U.S. Food and Drug Administration (FDA) has strict requirements in place for clinical data of studies carried out in China.

There has also been a lot of uncertainty around the ADR delistings of Chinese companies in the U.S. Further, biotech firms have seen poor IPO (initial public offering) performance in the last two years. All these factors have been pulling down the stock since its listing in January last year, Zelin said.

Meanwhile, the company plans to submit clinical data from a trial conducted in China in its Investigational New Drug (IND) filings to the FDA. If the U.S. regulator rejects the data, it could result in further downside for the stock, the analyst added.

How Well is Gracell Funded?

Gracell ended last year with $288 million in cash and short-term investments.

Commenting on the company’s funding, the analyst said, “We see Gracell in a comfortable and stable financial position with sufficient cash runway through inflection points in both lead clinical programs (GC012F and GC027).”

Basis of Gracell’s Valuation

Zelin has set a price target of $18 for Gracell, as he expects the company to receive regulatory approval for GC012F in the U.S. and China in 2025 and in the European Union (EU) in 2027. He also expects GC027 to get a green light in the U.S., EU, and China in 2025.

The valuation is based on a discounted cash flow (DCF) analysis with a discount rate of 12% and a terminal growth rate of 2%.

Overall, the stock has a Moderate Buy consensus rating based on two Buys. GRCL’s average price target of $21.50 implies 711.3% upside potential.

Apart from Zelin, Joseph Catanzaro of Piper Sandler (NYSE: PIPR) is the only analyst who has provided coverage on the stock. Catanzaro has a Buy rating on GRCL with a price target of $25 (843.4% upside potential).

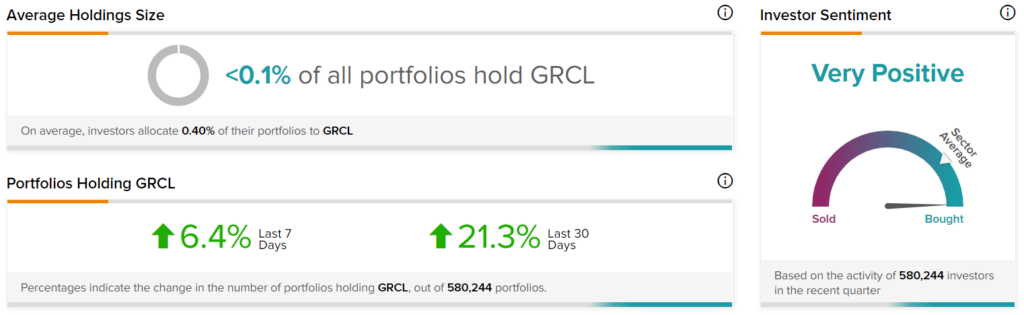

Positive Investor Stance

TipRanks’ Stock Investors tool shows that investors currently have a Very Positive stance on Gracell, as 21.3% of investors on TipRanks increased their exposure to the stock over the past 30 days.